**The Gravity of Reality: Unpacking the "Space Beach" Asteroid Mining Boom**

**Corporate pitch decks project astronomical wealth, but the math tells a much more sobering story.** Startups are aggressively marketing the financial promise of deep space. AstroForge boasts that asteroid mining is a "$1 Trillion" economy with staggering 85% profit margins on Platinum Group Metals. Similarly, executives at ExLabs predict the industry will eventually "total billions of dollars" and reverse Earth's supply chain entirely.

However, a techno-economic analysis reveals that flooding the terrestrial platinum market with space-mined metals would likely crash the price of the commodity, as the market is highly inelastic. The operation would only remain profitable if Earth-based production decreased proportionately to offset the new supply. Furthermore, to simply break even on a platinum mining mission, a spacecraft would need an incredibly high throughput rate, requiring it to process the equivalent of its own mass in just three seconds.

**There is a massive gulf between the ambitious promises of these startups and their actual technological track records in orbit.** ExLabs operates out of a Long Beach warehouse with around a dozen employees, yet it promises to launch a spacecraft in 2028 to intercept the asteroid Apophis 100 million kilometers away in 2029. Meanwhile, AstroForge has already experienced significant orbital failures. Their first spacecraft, Brokkr-1, was launched in 2023 with a magnetic field defect that the company knew about prior to liftoff; they chose to launch anyway to avoid delays and costs, resulting in severe orientation and communication issues. Their second mission, Odin, was completely rebuilt in-house after failing vibration tests, launched on February 27, 2025, and was officially declared lost just weeks later on March 6, 2025, due to ground station and communication failures.

**Despite the "commercial" branding, much of this industry is heavily underwritten by the public sector.** TransAstra recently received a $2.5 million contract from NASA to scale its inflatable "Capture Bag" technology. ExLabs relies on a patchwork of grants and contracts from NASA, the U.S. Space Force, the Air Force, and JPL. Even heavily capitalized companies like Vast Space benefit from an "Unfunded Space Act Agreement" with NASA, which grants them vital access to government technical data, lessons learned, and facilities without the direct transfer of funds.

**While these companies rely on public support, the U.S. government is actively rushing to deregulate their activities.** Because current licensing regimes do not adequately cover activities like space resource extraction, the Department of Commerce's Office of Space Commerce (OSC) is proposing a new "Space Commerce Certification". This proposed framework features a "light-touch" approach with a "presumption of approval" and a strict 120-day shot clock for decisions. This raises critical questions about whether such fast-tracking is safe, especially given that companies like AstroForge have demonstrated a willingness to launch known defective hardware.

**Ultimately, this speculative ecosystem is heavily promoted by local politicians and academic institutions desperate for economic revitalization.** Following the 2015 closure of the Boeing C-17 Globemaster III plant, the city of Long Beach actively rebranded itself as "Space Beach" to drive post-COVID economic recovery. Local institutions like California State University, Long Beach (CSULB) heavily subsidize the industry's recruitment efforts by churning out 1,200 engineering graduates annually, acting as the primary talent pipeline for these high-risk space ventures.

The Celestial Supply Chain: An Industry Intelligence Report on AstroForge and the Asteroid Mining Frontier

1. Executive Summary: The Reversal of Earth’s Supply Chain

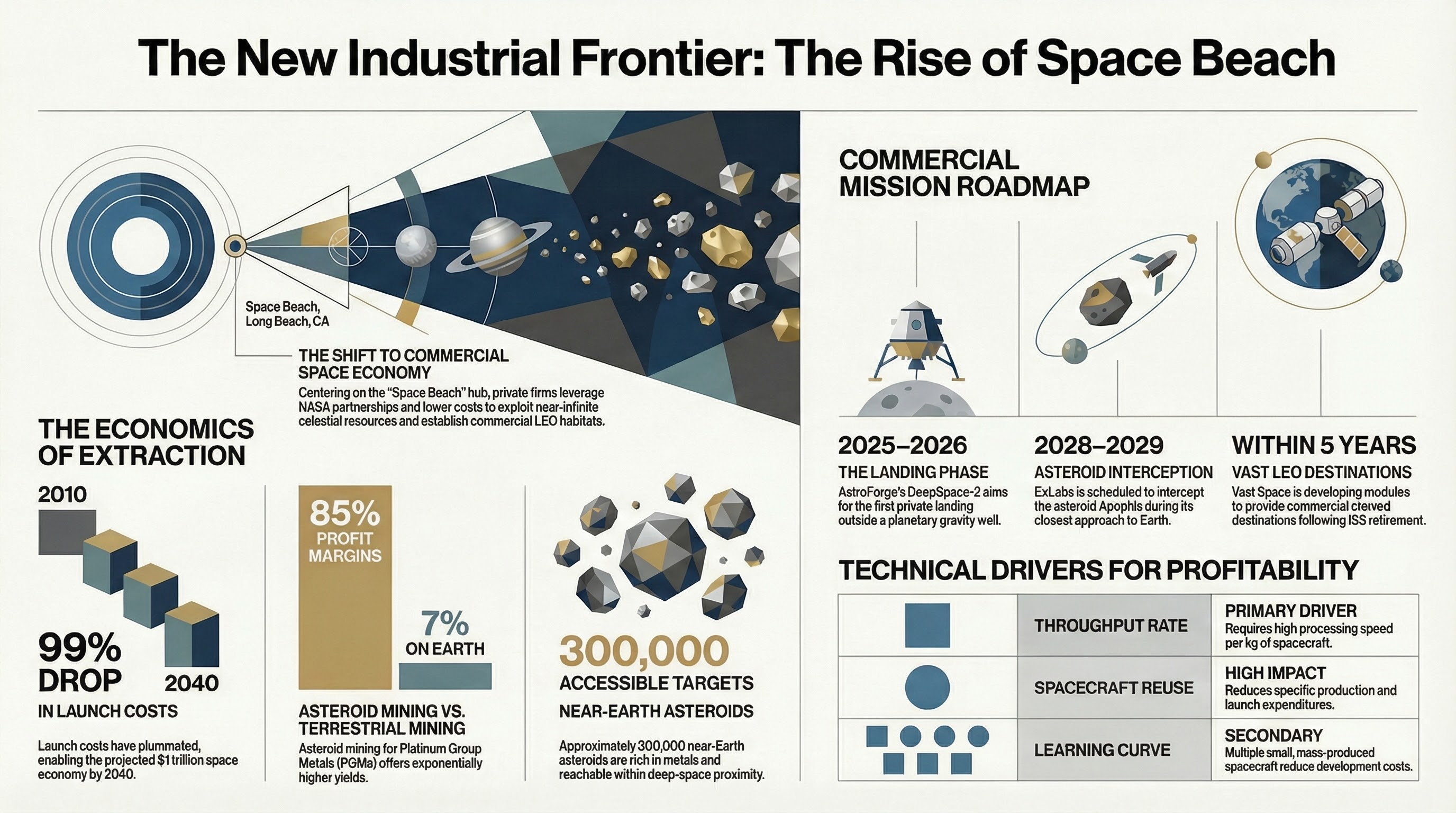

The global logistics paradigm is currently undergoing a fundamental "reversal." For decades, the terrestrial supply chain for high-value minerals has been characterized by diminishing returns, ecological degradation, and geopolitical volatility. The transition toward space-based resource extraction represents a strategic pivot where the primary source of raw materials moves from the Earth's crust to Near-Earth Asteroids (NEAs). This shift is not a speculative venture but a techno-economic necessity for sustaining a projected $1 trillion space economy by 2040.

Table 1: Trillion-Dollar Industry Drivers

Economic Catalyst Data Point / Metric Strategic Impact

Launch Cost Optimization 99% reduction in $/kg since 2010 Lowers the entry barrier for high-frequency industrial hardware deployment.

Resource Abundance ~300,000 metal-rich asteroids in proximity Provides virtually infinite supply of PGMs, addressing 200+ years of global demand.

Market Expansion $1T projected valuation (2040) Signals a transition from institutional research to commercial heavy industry in LEO and beyond.

The foundational driver for this reversal is the margin disparity between terrestrial and orbital extraction. Earth-based Platinum Group Metal (PGM) mining is burdened by high energy costs and environmental remediation, yielding slim margins of approximately 7%. In contrast, asteroid-based PGM operations are projected to reach 85% margins. This profitability is predicated on the extreme mineral concentration of M-type bodies, which allows for significantly higher yields per kilogram of processed material. Realizing these margins, however, remains contingent on overcoming substantial technical hurdles in autonomous deep-space refinement.

2. Corporate Profile: AstroForge and the M-Type Ambition

AstroForge, established in 2022, has adopted a high-value, high-risk strategy by targeting M-type (metallic) asteroids exclusively. While competitors focus on water extraction for propellant—a market currently limited by lack of orbital infrastructure—AstroForge targets the immediate terrestrial demand for PGMs. Their operations focus on Near-Earth Asteroids (NEAs) ranging from 20 to 300 meters in diameter, which constitute approximately 3–5% of the NEA population. The firm utilizes an in-house, 3D-printed spacecraft philosophy to achieve a "low-cost, replicable" fleet, avoiding the multi-year lead times of custom-built deep-space probes.

AstroForge Norse-Themed Mission Roadmap

* Brokkr-1

* Status: Launched (April 2023); Mission Terminated.

* Objective: In-orbit testing of PGM vaporization and refinement technology in LEO.

* "So What?" Analysis: The mission failed due to magnetic field interference from the refinery system, which disabled the cubesat’s orientation sensors. Crucially, the firm identified this risk pre-launch but made a calculated risk-to-capital decision to proceed rather than face a nine-month delay. This demonstrates a venture-capital-driven "fail-forward" mentality where launch schedule is prioritized over total risk mitigation.

* Odin

* Status: Launched (February 26, 2025); Declared Lost (March 6, 2025).

* Objective: Deep-space flyby of asteroid 2022 OB5 to confirm metallic composition and capture high-resolution imagery.

* "So What?" Analysis: While officially declared lost due to ground station failures, the resilience of the hardware was evidenced by "sporadic communication" with an amateur radio operator in Germany post-failure. The primary learning is the vulnerability of the ground segment rather than the spacecraft bus, necessitating a more robust, decentralized communication architecture for the 2026 window.

* DeepSpace-2

* Status: Planned (H1 2026).

* Objective: The first private landing/docking on a metallic body to initiate extraction.

AstroForge's reliance on standardized buses addresses the high capital expenditures traditionally associated with deep space, shifting the focus toward capture-focused methodologies employed by peers.

3. Capture and Interception: The ExLabs and TransAstra Methodologies

Intercepting a Near-Earth Asteroid is frequently described as "shooting a bullet with another bullet." For the 2028 Apophis mission, this involves closing a gap between a spacecraft the size of a trailer and an asteroid as tall as the Empire State Building, both traveling at 7,000 mph. This level of precision requires autonomous navigation systems capable of operating under the significant signal delays inherent in heliocentric orbits.

ExLabs Strategy: The Apophis Window ExLabs is targeting the April 2028 launch window to intercept the asteroid Apophis during its 32,000 km close-approach to Earth in 2029. This mission intends to deploy payloads directly onto the surface to study the asteroid’s internal structure as it is stressed by Earth’s gravity field. Beyond structural analysis, the mission serves as a prospecting precursor for cobalt, platinum, chromium, and gallium—a critical mineral for high-performance electronics.

TransAstra Strategy: The Capture Bag System TransAstra is developing mechanical enclosure systems, recently securing a 5M contract (2.5M NASA CCRPP / $2.5M private) to scale their inflatable "Capture Bag" from 1 to 10 meters. This technology is strategically dual-purpose: the 1-meter variant addresses Kessler Syndrome by capturing orbital debris, while the 10-meter variant is designed to enclose small asteroids.

These capture technologies are the critical enablers for the celestial supply chain. By stabilizing iceless, rocky bodies that are in high-velocity transit or high-frequency spin, firms can transition from flyby observations to stable, long-duration mining and refinement.

4. Techno-Economic Analysis: The Profitability Threshold

In asteroid mining, profitability is governed by the "throughput rate"—the mass of material processed per second relative to the spacecraft's dry mass. This variable determines if a venture can reach breakeven before its operational capital is depleted.

Asteroid Mining Economic Comparison

Metric Water Mining (Conservative) Platinum Mining (Optimistic)

Throughput Rate Req. 2.3 * 10⁻⁴ kg/s/kg 0.035 kg/s/kg

Conservative Throughput Req. N/A 0.35 kg/s/kg

Years to Breakeven 5.9 Years 0.25 Years

Bootstrapping Factor 14.3 0.2

Note: Bootstrapping Factor is defined as the ratio of mass return to spacecraft dry mass.

Price Elasticity and External Volatility A significant market risk is the "linear supply-demand curve." If a mining venture floods the market with platinum, the resulting price collapse could negate the NPV of the mission. Profitability exists within a slim elasticity range (0.25 to 0.9). Furthermore, external shocks—such as the Volkswagen diesel scandal reducing PGM demand or the volatility of the South African Rand supporting terrestrial margins—can shift the profitability threshold unexpectedly. To survive, asteroid mining must act as a substitution for terrestrial mining rather than an additive source.

Six Technical Levers for Profit

1. Multiple Spacecraft: Using fleets to exploit learning curve effects and reduce per-unit development costs.

2. Throughput Optimization: Closing the gap between the optimistic 0.035 and conservative 0.35 kg/s/kg requirements.

3. Mission Compression: Launching subsequent spacecraft before previous missions return to maximize capital utility.

4. Spacecraft Reuse: Re-tasking hardware for multiple cycles to amortize launch costs.

5. Learning Curves: Achieving ~23% cost reductions as production volume doubles.

6. Expendable Efficiency: Utilizing low-cost expendable craft to enable tighter mission sequencing when reuse turnaround is too long.

5. Infrastructure and Logistics: Vast Space and the LEO Ecosystem

The celestial supply chain requires mid-stream waypoints in LEO to process or transfer returned materials. Vast Space is developing the infrastructure to support these logistics through artificial gravity modules, solving the biological and mechanical limitations of microgravity environments.

Vast Space / NASA Space Act Agreement (SAA-UA-23-38921) Milestones

* December 2025: Launch of the Sub-Scale Demo Module to verify automated systems and internal pressures (Milestone #12).

* March 2026: Conduct of a Private Crew Mission (2-4 individuals) to test docking and ingress (Milestone #14).

* July–October 2026: Orbital spin tests to demonstrate fractional and full RPM.

* March 2028: Completion of the Full-Scale Demo Module Test Readiness Review (Milestone #21).

* April 2028: Full-Scale hardware-in-the-loop mission simulation (Milestone #22).

The "Vast Primary Station" is designed as a long, spinning structure that provides 1G at its extremities with a range of partial gravity waypoints. These waypoints emulate Moon, Mars, and asteroid gravities, providing essential logistics hubs for industrial space work and medical response for deep-space personnel.

6. The Ecosystem: "Space Beach" and Regulatory Evolution

The concentration of asteroid mining talent in Long Beach, California—known as "Space Beach"—has created a self-sustaining innovation ecosystem. With CSULB graduating 1,200 engineers annually and the co-location of SpaceX, Boeing, AstroForge, and ExLabs, the region facilitates a rapid workforce pipeline and localized supply chain.

Regulatory "Shot Clock" Framework To mitigate the "mission authorization gap" for resource extraction, the Office of Space Commerce (OSC) has proposed a "Space Commerce Certification" framework. This represents a passive process characterized by a presumption of approval:

* 30-Day Interagency Review: Stakeholders (NASA, DoD) must identify specific, compelling risks within a firm window.

* 120-180 Day Final Decision: A definitive timeline for applicants to receive certification.

* Presumption of Approval: A "light-touch" stance where authorization is granted unless it violates international obligations or poses unacceptable safety risks.

This regulatory evolution provides the legal certainty necessary for institutional investors to fund the 2026–2029 operational window. As Vast Space matures LEO waypoints and AstroForge/ExLabs execute interception missions, the celestial supply chain is transitioning into a functional reality for the global economy.